Railroad Logistics In Brazil: Usefull Information For Foreign Investors

Adler Martins*

Nayara Gonçalves**

Foreword

Foreword

Brazil has a great territorial extension and an increasing economic relevance in the world. Its GDP and exports have been growing consistently in the last decade, pushed particularly by the international demand for iron ore and agricultural products.

Brazil is also one of the main destinies for foreign investments in the world, having received over 34 billion dollars in direct investments in 2007.

To any company interested in investing in Brazil, knowledge about the intricate logistic network is invaluable. Even more if the target activities are logistics-dependent, such as mineral extraction. This brief article aims at providing broader and safer data on the subject, in order to support strategic business decisions.

History

The Brazilian railroads cover 28.5 thousand km (177 thousand miles) and are responsible for about 20% of the Brazilian cargo transportation matrix1. The Brazilian railroads have been basically built between 1850 and 1953. Its primary goals included the transportation of commodities such as sugar, coffee, iron ore and coal.

On the beginning of the 20th century, many Brazilian railroads systems started presenting operational losses, which lead some of them to bankruptcy. Among the reasons to this scenario, it is possible to point out the technologic obsolescence, the end of economic circles of certain products, as coffee, which demanded most part of the railroad services and the political preference for the Road transportation, which was largely stimulated by the federal government at the time.

To prevent the vicious consequences that would follow the extinction of too many railroad systems, the federal government decided to centralize and take control over the national railroad operations. Consequently, the Federal Railroad Network Corporation (RFFSA in the Portuguese acronym) was founded in 1957, with the purpose of making the railroad exploration the more efficient as possible, reducing the operational deficits. This new company absorbed most of the pre-existent Brazilian railroads.

Despite the initiative, there were no substantial investments in renovation or expansions of the railroad system since the middle of the 20th century. The demand for transportation services, however, has grown almost exponentially ever since. As a result, the national railroad system is, nowadays, a real obstacle to the efficiency of the Brazilian transportation infrastructure. The railroads currently operating are incapable of supplying the demand. That is especially true when it comes to mining activities.

In the early 90s, the Federal Government realized that it could not obtain the resources demanded by the railroads improvement program on the pace required by the national industry. Shortly after, a privatization program was launched as an option to handle the problem, or at least alleviate it.

The RFFSA was included on the National Denationalization Program through the Federal Decree n. 473 from 1992. The Decree established that the railroad exploration would be granted to private groups for 30 years, which could be extended for another 30.

Given the complexity and extension of RFFSA’s assets, the company has not been sold as a sole enterprise. Instead of that, a special commission divided the company in several smaller routes, each one being auctioned independently to.

Vale do Rio Doce – CVRD (nowadays Vale) is one of the companies that obtained public concessions to operate the system. The group became responsible for exploring two important tracks: the Carajas railroad and the Vitoria-Minas railroad. Those roads connect the Carajas and Minas Gerais mineral deposits to the Sao Luiz and Tubarao ports, respectively.

It should be stressed that Carajas is one of the richest mineral provinces in the world. Moreover, the so called “Iron Square”, in the Minas Gerais State, is the major mining region in Brazil. Therefore, the two railroad tracks controlled by Vale are crucial for the proper distribution and exportation of the Brazilian iron ore.

The Middle West and Sao Paulo tracks (Operated by Novo Oeste, Ferronorte and Ferroban railroads) have been granted to a group composed by CVRD, Previ (a pension fund owned by Banco do Brasil, an important Brazilian bank), Funcef (another pension fund), LAIF(Latin American Investment Fund) and JP Morgan Partners.

America Latina Logística (known as ALL) obtained control of the south track, which comprises Rio Grande do Sul, Santa Catarina and Parana states, what is to say, the whole south of Brazil.

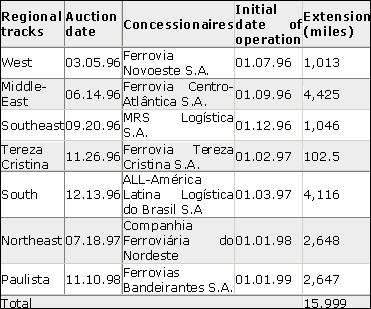

All railroad concessions to private companies have been auctioned according to the proceedings established by the bill n. 8.987, from 1995. The public auctions took place between 1996 and 1998.

The seven tracks described on the table below derived from the denationalization of the RFFSA, and have had its exploration rights granted for a 30-year period. These companies, however, do not own the railroad physic assets. Only Vale and Ferronorte effectively own the rails, terminals and locomotives from the tracks they explore.

The ANTT (Agência Nacional de Transportes Terrestres) is the government agency responsible for regulating terrestrial transportation in Brazil. Apart from previous RFFSA’s tracks and Vale’s railroads (which have been portrayed above), ANTT also rules the following concessions:

Ferrovias Norte Brasil S.A. - FERRONORTE.

-

Estrada de Ferro Mineração Rio do Norte;

-

Estrada de Ferro Jarí;

-

Estrada de Ferro Trombeta;

-

Estrada de Ferro Votorantim;

-

Estrada de Ferro Paraná Oeste S.A. – FERROESTE

The map below displays the current situation of the railroad concessions in Brazil:

Important information for foreign investors:

In the last years, Brazil has received huge amounts of direct foreign investments, mostly on metallurgy, mining and agriculture. In 2007 alone, foreign resources on the amount of US$4,699 billion have been invested in metallurgy and US$3,249 billion in the mining section.

The situation in mirrored in Ethanol and Biodiesel sectors, which have also attracted the interest of international investors.

In common, all these sectors share an accented dependence on the railroad logistics for its economic feasibility. It is, therefore, natural that the foreign investor be worried about the transportation of its products. At this point, many doubts about the Brazilian railroad system may appear.

Brazil adopted a sui generis system of railroad regulation. Here, the company that controls the most important railroad lines for mining exploration (the Carajás railroad, on north, and the Vitória Minas railroad, linking Minas Gerais to Vitória port) is, itself, a great mining company (Vale) and uses almost all the current capacity of the track it controls. In fact, the railroads controlled by Vale do not have enough capacity to supply its own demand.

The same is true in the case of others concessionaires that also depend on the railroads to fulfill their own commercial objectives. (The southeast track, for instance, is controlled by MBR and CSN, companies from mining and steel sectors).

The current situation reflects a truly impasse. In one side, the current situation favors almost monopolistic market control by Vale and CSN, since those private groups have control over a transportation modal which is vital for their competitors’ activities.

In such situation, it’s clear that only companies that control railroads tracks will be able to survive. On the off side, small companies will become completely vulnerable and dependent on the bigger companies.

On the other hand, it’s important to consider that, without the denationalization program, it is probable that not even the big companies would have conditions to operate competitively on the international market. In fact, the deficiencies caused by the lack of governmental investments on the railroads have been almost catastrophic to Brazil.

Sector regulation and legal alternatives to secure the use of railroads

Despite being apparently disheartening, the logistics obstacle is not an insuperable problem for those who whish to invest on highly logistics-dependent sectors.

In some situations, there are legal instruments that can ensure the use the railroads. Moreover, there are also other solutions that will be explored later on this text.

As for the use of the railroads, it must be said that, despite the popular opinion, the logistic operators cannot freely establish the freight prices. The concession contracts entered into among the government and the concessionaries clearly establish, on its seventh clause, that the maximums prices practiced by the concessionaries will be established by ANTT.

Indeed, the ANTT establishes different prices for each class of goods, such as coal, ore, grains, etc. Thus, it is possible to accurately calculate the final freight cost for virtually any product.

Still, experience has demonstrated that the freight prices are not the only problems when it comes to analyzing investment opportunities in logistics-dependent sectors.

Rather, it is the lack of available wagons for the transportation of the goods that causes most of the insecurity. More often than not, the concessionaires are so overloaded with their own cargo that they cannot supply continuous services to other users.

However, it is possible to appeal to ANTT protection to force the logistic operators to reserve a certain number of wagons for the transportation of goods belonging to companies with extreme dependence on public railroad services.

The legal concept of “user with high dependence on public railroad services” has been described on the railroad concession contracts entered into from 1996 on. However, only as for 2004 has ANTT decisions been favorable to this kind of user. The recognition of the high dependence is able to obligate the operator to charge lower prices when dealing with that specific user. The recognition may also include a transportation warranty, although restricted.

Some successful cases based on this legal remedy include agreements between users and operators, according to which the user company shall donate the wagons that will be utilized for transporting its products.

This possibility, however, should not be considered as a panacea. The high dependence recognition is subject to prior and strict analysis by ANTT. Moreover, railroad capacity limitations may make it impossible for the concessionaries to secure transportation in the level required by the claimant company.

The Brazilian market has recently watched a bold and creative initiative, aiming at overcoming the logistic limitations imposed to mining activities.

MMX Minas Rio, a Brazilian mining corporation, has started the construction of a 530 km (331 miles) mining pipeline, connecting a mine in the city of Conceição do Mato Dentro, in Minas Gerais state (center of Brazil), to the coast. The company is also building an exclusive port in Rio de Janeiro state to handle the exportation of its production.

This very ambitious project, with total cost estimated in US$2.3 billion dollars revealed the existence of feasible solutions to overcome the knot on Brazilian logistics.

Final word

Brazil has countless investment opportunities on logistics dependant sectors. To efficiently explore those activities, any project shall be carefully analyzed, taking in account all legal and economic alternatives.

Through the wise utilization of the available legal resources, the obstacles that trouble many companies may be turned into a competitive advantage to the prepared ones.

_____________

1 (Click here)

table: Source: ANNT. Available at (Click here)

map: Source: ANNT. Available at (Click here)